What To Know About Investing in Short-Term Rental Properties

Many people are looking for a way to diversify their investments, and real estate investing is a popular option. Some people might be interested in short-term rental properties. What is a short-term rental property, and what are the responsibilities of property owners? Learn more about short-term rental properties to figure out if this is a solid option.

Many people are looking for a way to diversify their investments, and real estate investing is a popular option. Some people might be interested in short-term rental properties. What is a short-term rental property, and what are the responsibilities of property owners? Learn more about short-term rental properties to figure out if this is a solid option.

An Overview Of A Short-Term Rental Property

A short-term rental property is a rental property that typically has residents and renters for fewer than 12 months at a time. Many people believe that short-term rental properties are vacation homes and Airbnb-type properties; however, just about any property can be a short-term rental. This includes a condo, a townhome, or a single-family home. Typically, the owner of a short-term rental property doesn’t live in it but rents it out to people for a few days, weeks, or months at a time.

The Responsibilities Of A Short-Term Rental Property Owner

There are many responsibilities that come with owning a short-term rental property. Many of them are similar to the responsibilities of owning a long-term rental property; however, because there is more turnover, these responsibilities tend to arise with greater frequency.

For example, short-term rental property owners need to screen everyone who applies to stay at the property. The property owner is typically responsible for utility bills as well, as the renters do not stay there long enough to develop a relationship with a utility company. Short-term property owners also need to keep a close eye on their records to make sure they keep track of their income and overhead expenses.

Maximizing Income In A Short-Term Rental Property: Take Care Of It

There are several ways short-term rental property owners can maximize their income. They need to select a property that is in a favorable location with a lot of interest. Then, they need to take care of the property to make guests feel welcome. Purchasing some nice furniture, handling maintenance on time, and advertising the property on social media can drive up demand and interest. These are the best ways to maximize income on a short-term rental property.

If you want to save money on your mortgage, refinancing your house could be a great move. As long as you have plenty of equity and a great credit score, you should be able to qualify for the refinance process. At the same time, you might be wondering, how long will it take you to refinance your house? There are several factors to keep in mind, so be sure to work with a professional who can walk you through the process.

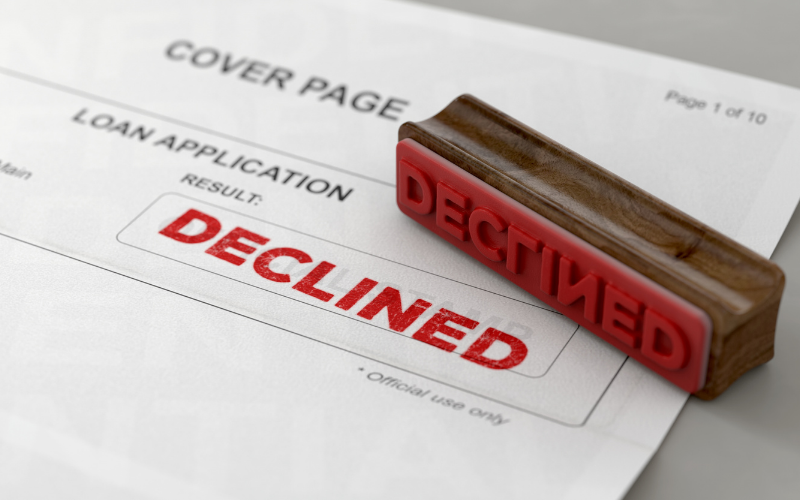

If you want to save money on your mortgage, refinancing your house could be a great move. As long as you have plenty of equity and a great credit score, you should be able to qualify for the refinance process. At the same time, you might be wondering, how long will it take you to refinance your house? There are several factors to keep in mind, so be sure to work with a professional who can walk you through the process. If you want to save money on your home loan, you might want to refinance. During the refinancing process, you could secure a better interest rate on your home loan. You could also withdraw cash from your home’s equity value to cover other expenses. Similar to a regular mortgage application, some refinance applications are denied. Why is this the case, and what should you do next?

If you want to save money on your home loan, you might want to refinance. During the refinancing process, you could secure a better interest rate on your home loan. You could also withdraw cash from your home’s equity value to cover other expenses. Similar to a regular mortgage application, some refinance applications are denied. Why is this the case, and what should you do next?