Facing Foreclosure? Here’s What It Means–and What You Can Do About It

If you’re a homeowner, foreclosure is one of those things you hope you never have to think about. But if payments start getting tight, it can suddenly feel very real—and very overwhelming.

If you’re a homeowner, foreclosure is one of those things you hope you never have to think about. But if payments start getting tight, it can suddenly feel very real—and very overwhelming.

The good news? Foreclosure doesn’t happen overnight, and you usually have more options than you think.

Let’s break down what’s actually happening and what you can do to stay ahead of it.

What Is Foreclosure (Really)?

Foreclosure is the process a lender uses to recover the money they loaned you if mortgage payments stop.

In simple terms:

If payments aren’t made over time, the lender can take legal steps to sell the home and recover what’s owed.

It sounds intense—and it is—but it’s typically a process, not a single event. And that process creates opportunities to act before things escalate.

How the Process Usually Unfolds

While timelines vary by state, foreclosure generally follows a pattern:

- Missed payments begin to add up

- You receive notices from your lender

- A formal notice of default may be issued

- There’s a window of time to catch up or make arrangements

- If unresolved, the home may eventually be sold

The key takeaway: there’s usually a gap between “things are slipping” and “you’re out of options.”

That gap is where your leverage is.

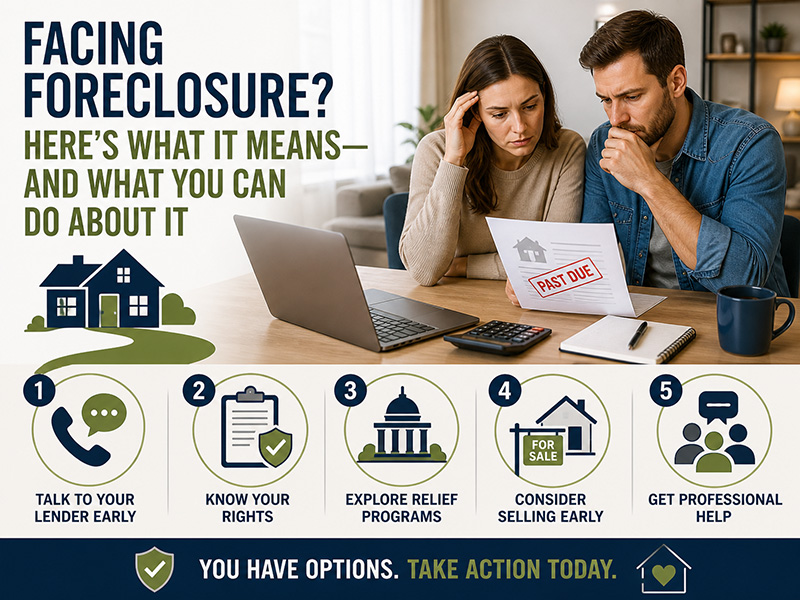

5 Smart Ways to Avoid Foreclosure

1. Talk to Your Lender Early (Not Late)

This is the one people avoid—and it’s the one that helps the most.

Lenders don’t want to foreclose. It’s expensive and time-consuming for them too. If you reach out early, they may offer options like:

- Payment plans

- Loan modifications

- Temporary forbearance

The earlier the conversation happens, the more flexibility you’ll have.

2. Get Clear on Your Timeline

Uncertainty makes everything feel worse.

Take the time to understand:

- How many payments you’ve missed

- What notices you’ve received

- What your state’s foreclosure timeline looks like

Knowing where you stand helps you move from panic → strategy.

3. Look Into Relief & Assistance Programs

There are often programs—federal, state, or local—that can help bridge the gap.

These may include:

- Refinancing options

- Payment assistance

- Temporary hardship programs

Some come and go depending on the economy, so it’s worth checking what’s currently available.

4. Consider Selling Before It Becomes Urgent

If keeping the home isn’t realistic long-term, selling before foreclosure can protect your finances and your credit.

It also gives you:

- More control over timing

- A better chance at maximizing value

- A cleaner transition overall

Waiting too long can limit your options, so this is one to think about early, not last-minute.

5. Talk to a Professional (You Don’t Have to Navigate This Alone)

There are people whose entire job is to help in situations like this.

That might include:

- A HUD-approved housing counselor

- A real estate professional

- A financial advisor

Getting guidance can help you see options you might not have considered and take some of the pressure off figuring it all out solo.

The Bottom Line

Foreclosure is serious, but it’s not instant, and it’s not inevitable. The biggest difference-maker? Taking action early.

Even small steps—like making a phone call or reviewing your options—can shift things in your favor and give you more control over what happens next.