What Mortgage Lenders Really Look At Before Approving Your Loan

One of the first questions homebuyers ask is how much they can afford to borrow. While the number may seem mysterious, lenders use a clear set of financial factors to decide how much you qualify for.

One of the first questions homebuyers ask is how much they can afford to borrow. While the number may seem mysterious, lenders use a clear set of financial factors to decide how much you qualify for.

Understanding these factors can help you plan ahead, make smart choices, and feel confident as you start your homebuying journey.

Your Income and Employment History

Lenders begin by reviewing your income to determine if it is stable and sufficient to support a mortgage payment. They will verify your employment history, pay stubs, tax returns, and other documentation to confirm consistency. A steady income reassures the lender that you can manage monthly payments without financial strain.

vYour Debt-to-Income Ratio

Your debt-to-income ratio, or DTI, is one of the most important calculations in the loan process. It measures how much of your monthly income goes toward paying existing debts, including credit cards, student loans, car payments, and any other obligations. A lower DTI shows that you have room in your budget for a new mortgage, which can increase your borrowing power.

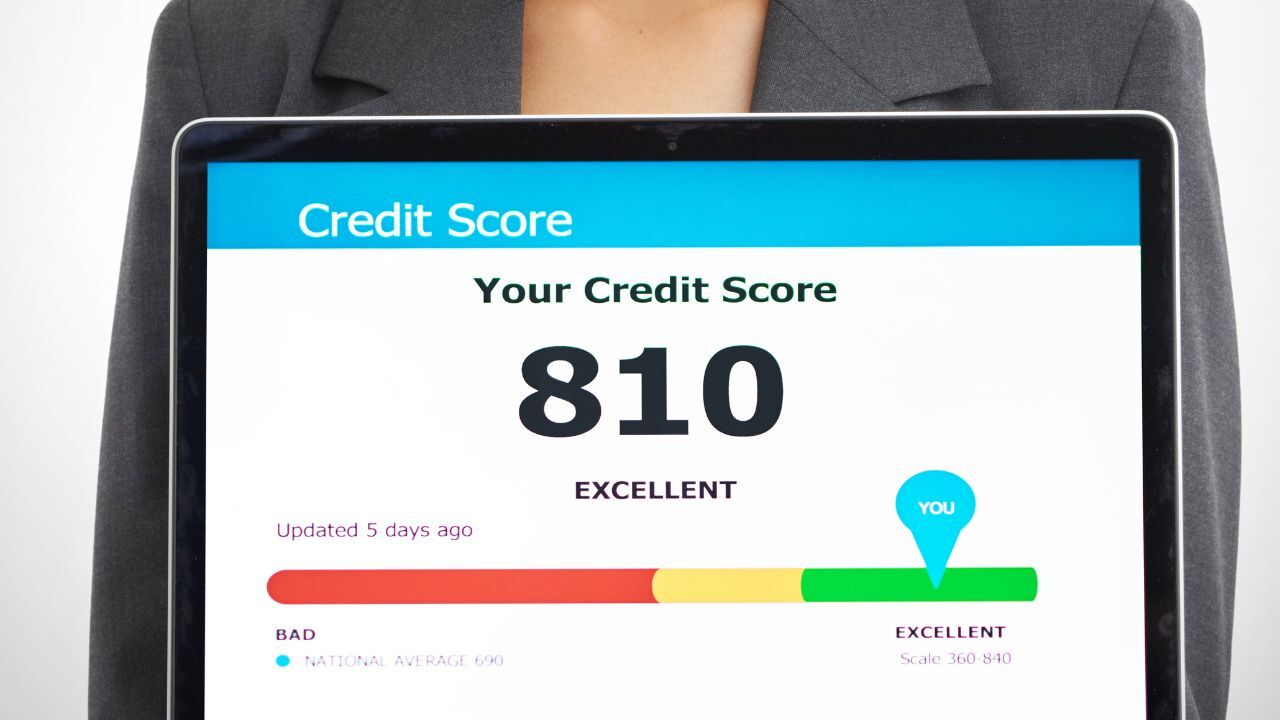

Your Credit Score and History

Credit plays a major role in the amount you can borrow and the interest rate you receive. A higher credit score tells lenders that you manage your finances responsibly and are likely to make timely payments. If your score is lower, lenders may offer a smaller loan amount or a higher rate to offset the perceived risk. Building and maintaining good credit before applying for a mortgage can make a meaningful difference.

Your Down Payment

The amount you plan to put down directly impacts how much you can borrow. A larger down payment reduces the loan amount and shows that you have a financial investment in the property. It can also help you qualify for better terms and possibly eliminate the need for mortgage insurance.

The Property Itself

The value of the home you want to purchase also affects your loan amount. Lenders will require an appraisal to ensure that the propertyís market value matches or exceeds the price you have agreed to pay. This helps protect both you and the lender from overpaying.

Mortgage lenders look at your full financial picture to decide how much you can borrow. By understanding and preparing for these factors, you can set realistic expectations, strengthen your application, and position yourself for success when it is time to buy.

Buying a home is one of the most exciting goals you can set, but your credit score plays a major role in how easy or challenging the process will be. The good news is that with time and planning, you can strengthen your credit and set yourself up for a smoother approval when you are ready to buy next year.

Buying a home is one of the most exciting goals you can set, but your credit score plays a major role in how easy or challenging the process will be. The good news is that with time and planning, you can strengthen your credit and set yourself up for a smoother approval when you are ready to buy next year.