The Importance of Communication Between Mortgage Originators and Clients

Effective communication between mortgage originators and clients is essential in ensuring a smooth, stress-free home financing process. Purchasing a home is one of the biggest financial decisions a person can make, and navigating the mortgage process can be overwhelming. Strong communication helps clients understand their options, stay informed, and ultimately secure the best loan for their needs.

Effective communication between mortgage originators and clients is essential in ensuring a smooth, stress-free home financing process. Purchasing a home is one of the biggest financial decisions a person can make, and navigating the mortgage process can be overwhelming. Strong communication helps clients understand their options, stay informed, and ultimately secure the best loan for their needs.

Here’s why maintaining open and clear communication is vital in the mortgage process:

- Setting Clear Expectations — One of the biggest reasons for miscommunication in the mortgage process is a lack of clarity on what to expect. A mortgage originator should provide a roadmap of the entire loan process, from application to closing. Clients need to be aware of key steps, required documents, and potential challenges that may arise. By setting clear expectations upfront, mortgage professionals can reduce confusion and minimize delays.

- Reducing Stress and Anxiety — Applying for a mortgage can be a daunting experience, especially for first-time homebuyers. When clients do not receive timely updates, they may feel anxious about their loan approval status or next steps. Regular check-ins and proactive communication help ease worries and keep clients confident throughout the process. Whether through emails, phone calls, or online portals, keeping clients informed helps build trust and transparency.

- Avoiding Costly Mistakes and Delays — Miscommunication or lack of communication can lead to costly mistakes that delay loan approvals or even cause deals to fall through. Missing paperwork, incorrect financial information, or misunderstanding loan terms can create obstacles in the mortgage process. A mortgage originator who actively communicates and ensures clients understand all requirements can help prevent these issues before they become major problems.

- Educating Clients on Loan Options — Many borrowers are unaware of the different mortgage products available to them. Without clear guidance, they may settle for a loan that does not align with their financial goals. By taking the time to explain various loan options, interest rates, and down payment requirements, mortgage professionals empower clients to make informed decisions. Understanding the pros and cons of FHA, VA, USDA, or conventional loans can help clients choose the best fit for their needs.

- Building Long-Term Relationships — Strong communication fosters long-term client relationships. A mortgage originator who is responsive, knowledgeable, and approachable is more likely to earn repeat business and referrals. Homebuyers remember positive experiences and are more likely to recommend their mortgage professional to friends and family. Effective communication not only benefits the current transaction but also contributes to future business growth.

- Handling Changes in Loan Conditions — The mortgage process can be unpredictable, and sometimes interest rates, loan terms, or financial conditions may change. Clients need to be aware of any shifts that may affect their loan approval. Mortgage originators must be transparent about these changes and provide guidance on how to proceed. Prompt and honest communication ensures clients are prepared for any adjustments and can make necessary financial decisions accordingly.

- Enhancing Client Confidence and Satisfaction — A mortgage originator who prioritizes communication helps clients feel valued and understood. When borrowers receive timely responses and clear explanations, they gain confidence in their mortgage professional’s ability to handle their loan. This leads to higher client satisfaction, positive reviews, and increased credibility in the industry.

Communication is the foundation of a successful mortgage transaction. By keeping clients informed, setting clear expectations, and providing education on loan options, mortgage originators can create a smooth and efficient home-buying experience. Effective communication reduces stress, prevents delays, and builds long-term client trust.

Buying a home in a remote area can be a dream come true—peaceful surroundings, open spaces, and a slower pace of life. However, securing a mortgage for these properties comes with unique challenges. As a mortgage originator, I’m here to break down the hurdles and offer solutions so you can make your rural homeownership dreams a reality.

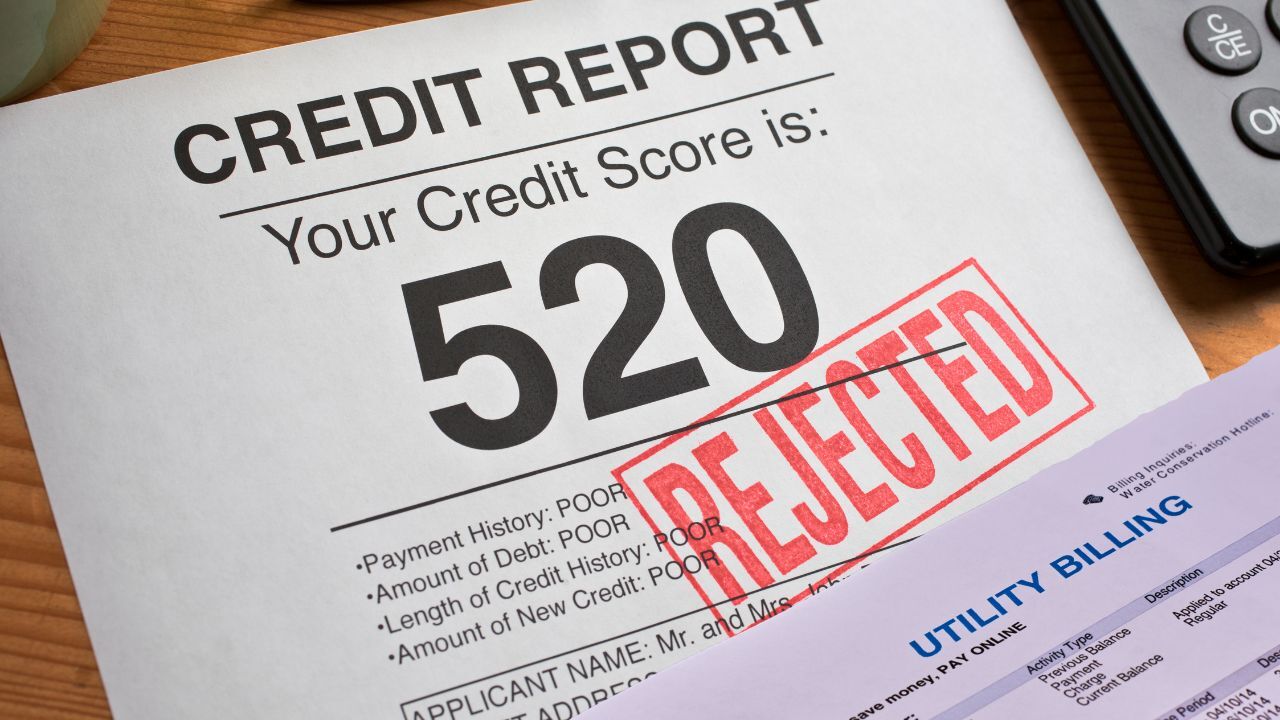

Buying a home in a remote area can be a dream come true—peaceful surroundings, open spaces, and a slower pace of life. However, securing a mortgage for these properties comes with unique challenges. As a mortgage originator, I’m here to break down the hurdles and offer solutions so you can make your rural homeownership dreams a reality. If you’ve been managing your finances responsibly but don’t have a traditional credit score, you may be wondering whether homeownership is still within reach. The good news? It is! While most mortgage lenders rely on credit scores to assess your creditworthiness, alternative credit history—like rent payments, utility bills, and other recurring expenses—can help you qualify for a mortgage.

If you’ve been managing your finances responsibly but don’t have a traditional credit score, you may be wondering whether homeownership is still within reach. The good news? It is! While most mortgage lenders rely on credit scores to assess your creditworthiness, alternative credit history—like rent payments, utility bills, and other recurring expenses—can help you qualify for a mortgage.